The Importance of Capital Efficiency in Corporate Venturing

‘Capital efficiency’ is increasingly seen by Venture Capital (VC) funds as a leading indicator of the return on investment over the life of a start-up. While not a new concept, it has gained in importance as start-ups face increasing scrutiny over indiscriminate expenditure on private jets and lavish parties, as well as public market skepticism over elevated private market valuations. While this emphasis on financial stewardship took hold in 2020 as investors pulled back amidst uncertainty around the developing COVID-19 pandemic, VC rounds remained smaller in 2021, even as other investment categories saw increased inflows¹ ².

It appears that a start-up’s capital efficiency is likely to remain a focus for investors.

So how should start-ups think about capital efficiency? There are a few ways:

- The ratio of Money raised (by any means), minus cash on balance sheet, to Revenues (i.e., (Total Equity + Total Debt — Cash) / Annual Revenue rate).

- The amount of money a company raises until it can be sustain itself on internally generated funds (i.e., Total Equity + Total debt needed until cashflow positive)³.

- The ratio of net burn to net New ARR (what David Sacks calls, the “Burn Multiple.”⁴, i.e., Monthly Burn / New Annual Recurring Revenue).

For this article, let us focus on the Burn Multiple, as it focuses on the ability of the money spent to generate new recurring “high quality” revenues.

David provides the following heuristic in his article:

Effectively, this suggests that burning about $1.50-$2.00 in a year to generate $1.00 of new recurring revenue per year is reasonable for a growing start-up. Burning less than that is impressive but burning more may be unsustainable, or at least a cause for concern. Furthermore, as a start-up matures, the Burn Multiple should become lower.

The importance of the Burn Multiple becomes clear when you consider what may be driving it:

- Inefficient sales. High expenditure on sales that is not effectively bringing in new revenue.

- No product-market-fit. The high cost of acquiring customers may suggest that product-market-fit has not yet been achieved.

- Inadequate margins. Customers are not willing to pay enough for a product or service.

- Stalling growth. Ever-increasing expenditure is required to maintain the same rate of growth.

- Undisciplined leadership. The management is unable or unwilling to control the burn rate.

While the specific elements contributing to a poor Burn Multiple may differ from venture to venture, the metric gives some indication of any venture’s capital efficiency.

As start-ups and VCs are beginning to learn the hard lessons of capital efficiency, many large corporations undertaking venture-building activities — ironically — have been slower to adopt this perspective. In our experience with large corporates, even those that monitor their capital performance, their ventures efforts often fall into the traps above, in addition to pitfalls that come specifically with the territory of corporate venture building.

For example:

- Failing to include the cost of idea generation and early development by third-party innovation consultants. For a short innovation exercise, these consultants often charge fees many times the annual expenditures of seed-stage start-ups. Furthermore, the business model of these consultants is seldom aligned with the long-term success of the venture, leading to venture ideas that look great on slide decks but do not stand up to the scrutiny of the market.

- Approving large amounts of funding too early, sometimes even before a relevant business plan has been validated. A VC-style funding strategy across several rounds would have better managed the risks by giving the corporate the opportunity to re-examine the results at various stage gates.

- Ignoring platform costs (including the innovation team, management bandwidth, internal development costs, etc.), especially when these costs often eclipse the funding or traction of the venture itself.

- Failure to align incentives with the operating team within the corporate, overestimating the future value of the venture, underestimating the risk, and not understanding the contributions required to achieve success.

As capital efficiency becomes more important for non-corporate ventures, corporates should better incorporate (pun intended) capital efficiency and the Burn Multiple into their venture building activities. This will allow corporates to manage their venture building portfolio with good risk management practices as opposed to starting the journey with an “innovation blank check” only to despair a few years later when the music stops. Beyond setting out clear terms of engagement for both founders and the venture, a proper venture risk management process will also ensure that the venture focuses on high-quality growth rather than vanity metrics. An outcome of this approach is that it will quickly separate the corporate venture founders who are truly entrepreneurial and are willing to align their success with the venture, from those who are very comfortable with their corporate salaries and perks and are unlikely to succeed outside the cocoon of corporate structure.

Capital efficiency becomes of paramount importance if the corporate wants the venture to attract investment from VC funds. In addition, for those ventures that the corporate is as yet unsure of the strategic value, or is leaning towards spinning them in, this metric ensures that the innovation effort is seen through an objective lens and not just as a qualitative experiment. As mentioned in our previous article The Strategy Case for Investible Ventures, corporates can increase capital efficiency of their ventures by helping them gain recurring revenues (hence lowering the Burn Multiple) through their corporate unfair advantage. Using the base Burn Multiple number as a benchmark can help the corporate identify the additional value it adds while justifying a higher valuation for the venture.

So as a corporate, how do you manage the Burn Multiple as part of your venture building exercise? By focusing on 4 key elements:

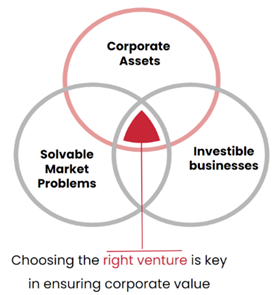

- Identify clearly what to build. Similarly for non-corporate ventures, solving a specific market problem by identifying clear pain points and solutions drives product-market fit, lowering the Burn Multiple for corporate ventures. An additional determinant for corporate ventures is the ability to utilize an unfair advantage conferred by the corporate (see picture above). At Wright Partners, we do not believe that the number of ventures that fit the above criteria is numerous, so choosing which venture to embark on is very important in achieving capital efficiency.

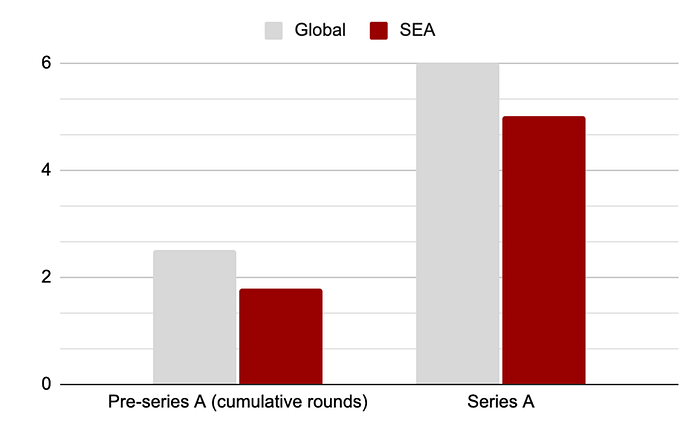

- Limiting the expenditure on the venture (including the ideation sprints and infrastructure costs allocated to a given venture). A start-up typically spends up to USD2 million to get to initial product-market fit before raising Series A investment (see picture above). Corporates should strive to achieve this too if they are seeking similar returns on their capital. Establishing such limits allows the corporate to benchmark its efforts against the market. In addition, it prevents the corporate venture founders from adopting a low-risk mindset that would hinder the venture from achieving its potential.

- Have a clear and efficient two-way governance system. It is important that the balanced governance system results in both the venture and the corporate being aligned in helping the venture succeed in the most capital-efficient manner.

- For the venture, the elements are very similar to those that govern the relationship between a VC and a start-up. These normally give a fair amount of operational control to the founders, while ensuring that the directors and the shareholders are consulted on pivotal matters.

- For the corporate, as ensuring capital efficiency requires leveraging corporate unfair advantages (e.g., access to customers, bundling with other corporate products), the governance system should encourage collaboration between the venture and the corporate divisions.

- Explicitly give incentives to both the corporate and venture actors to improve capital efficiency, while managing the risk-reward trade-offs.

4. Ensure that the best team is empowered and focuses on what matters, as an example from Aris Pattakos' article⁵.

- Get to market quickly through selling and getting feedback from real customers (through paid pilots as opposed to interviews).

- Solve problems in the fastest and best manner.

- Reaching customers who have the problem you hope to solve and get them to solve their problem by using your product.

At the same time, ensure that the team does not waste time on less relevant things.

- Spending too much time on generating buzz through news articles and other media before understanding what the company stands for and what it needs to sell.

- Spending too much time on navigating corporate compliance and corporate departmental politics — this usually results in death by a thousand cuts for a corporate venture

Capital efficiency is a great metric that corporates can use to manage its corporate venturing efforts. It mirrors how corporates already evaluate their business-as-usual operations while taking into account the specific elements that make venture building special. Keeping an eye on this important indicator will allow corporates to be significantly more successful while venture building.

Ziv Ragowsky, Founding Partner, Wright Partners

Tan Toi Ngee, Founding Partner, Wright Partners

Special thanks to Harry Schiff, Founding Member of Hitchhiker Ventures for his contribution to the article.

Sources

- https://insight.factset.com/venture-capital-2021-recap-a-record-breaking-year

- https://techcrunch.com/2022/03/16/new-data-shows-how-far-vcs-are-pulling-back-on-us-series-a-b-and-c-valuations/

- https://www.linkedin.com/pulse/capital-efficiency-startups-howard-love/

- https://medium.com/craft-ventures/the-burn-multiple-51a7e43cb200

- https://medium.datadriveninvestor.com/how-to-be-capital-efficient-when-building-your-startup-b40ff2ca61db